Older Entrepreneurs Leading the Way

We had the opportunity to talk with many great entrepreneurs doing research for our book, The New Builders. I was struck by how thoughtful, determined, and gritty they were. As most readers know, the book focuses on entrepreneurs from a diverse set of backgrounds – people that truly represent the next generation of founders in the United States.

One of the trends that we observe in the book is that the rate of entrepreneurship among older Americans is actually quite high. In fact, across all age groups, the fastest-growing group are entrepreneurs 55 and older. There are a number of interesting reasons for this that we talk about in the book. And we tell the stories of handful of older American entrepreneurs to help highlight these trends. One of my favorites was Fred Sachs who founded and eventually sold a lumber company as well as a commercial door and hardware company. He’s also my wife’s cousin, once removed (that’s her dad’s first cousin)!

Initially, Fred planned on retiring but his hobby of growing wheat on his farm near Alexandria, VA turned into a new venture selling flour to regional bakers. Grapewood Farm now produces a variety of organic small grains and stone ground flour to customers across the Mid-Atlantic region.

We highlight his story and the importance of older Americans in business in a piece in nextavenue that we just released this week. I hope you’ll check it out and see why our nation’s focus on Silicon Valley being the seat of innovation is not entirely on the mark.

Only an 8th grade education

Here’s the 8th grade competence exam from 1895. Thank god I went through 8th grade about 90 years later…

Hat tip to dad for sending this over.

Grammar (Time, one hour)

1. Give nine rules for the use of capital letters.

2. Name the parts of speech and define those that have no modifications.

3. Define verse, stanza and paragraph

4. What are the principal parts of a verb? Give principal parts of "lie", "play", and "run."

5. Define case; illustrate each case.

6. What is punctuation? Give rules for principal marks of punctuation.

7 – 10. Write a composition of about 150 words and show therein that you understand the practical use of the rules of grammar.

Arithmetic (Time, 65 minutes)

1. Name and define the Fundamental Rules of Arithmetic.

2. A wagon box is 2 ft. deep, 10 feet long, and 3 ft. wide. How many bushels of wheat will it hold?

3. If a load of wheat weighs 3942 lbs., what is it worth at 50cts/bushel, deducting 1050 lbs. for tare?

4. District No 33 has a valuation of $35,000. What is the necessary levy to carry on a school seven months at $50 per month, and have $104 for incidentals?

5. Find the cost of 6720 lbs. coal at $6.00 per ton.

6. Find the interest of $512.60 for 8 months and 18 days at 7 percent.

7. What is the cost of 40 boards 12 inches wide and 16 ft. long at $20 per meter?

8. Find bank discount on $300 for 90 days (no grace) at 10 percent.

9. What is the cost of a square farm at $15 per acre, the distance of which is 640 rods?

10. Write a Bank Check, a Promissory Note, and a Receipt

U.S. History (Time, 45 minutes)

1. Give the epochs into which U.S. History is divided

2. Give an account of the discovery of America by Columbus .

3. Relate the causes and results of the Revolutionary War.

4. Show the territorial growth of the United States .

5. Tell what you can of the history of Kansas .

6. Describe three of the most prominent battles of the Rebellion.

7. Who were the following: Morse, Whitney, Fulton, Bell, Lincoln, Penn, and Howe?

8. Name events connected with the following dates: 1607, 1620, 1800, 1849, and 1865.

Orthography (Time, one hour)

1. What is meant by the following: alphabet, phonetic, orthography, etymology, and syllabication.

2. What are elementary sounds? How classified?

3. What are the following, and give examples of each: trigraph, sub vocal, diphthong, cognate letters, and lingual.

4. Give four substitutes for caret ‘u.’

5. Give two rules for spelling words with final ‘e.’ Name two exceptions under each rule.

6. Give two uses of silent letters in spelling. Illustrate each.

7. Define the following prefixes and use in connection with a word: bi-, dis-, mis-, pre-, semi-, post-, non-, inter-, mono-, and sup-.

8. Mark diacritically and divide into syllables the following, and name the sign that indicates the sound:

card, ball, mercy, sir, odd, cell, rise, blood, fare, last.

9. Use the following correctly in sentences: cite, site, sight, fane, fain, feign, vane, vain, vein, raze, raise, rays.

10. Write 10 words frequently mispronounced and indicate pronunciation by use of diacritical marks and by syllabication.

Geography (Time, one hour)

1 What is climate? Upon what does climate depend?

2. How do you account for the extremes of climate in Kansas ?

3. Of what use are rivers? Of what use is the ocean?

4. Describe the mountains of North America 5. Name and describe the following: Monrovia , Odessa , Denver , Manitoba , Hecla , Yukon , St. Helena , Juan Fernandez, Aspinwall and Orinoco .

6. Name and locate the principal trade centers of the U.S.

7. Name all the republics of Europe and give the capital of each.

8. Why is the Atlantic Coast colder than the Pacific in the same latitude?

9. Describe the process by which the water of the ocean returns to the sources of rivers.

10. Describe the movements of the earth. Give the inclination of the earth.

PPP and Women and Minority-Owned Businesses – We Need To Do More

I’ve published a number of posts over the past few weeks about some of the challenges of the existing PPP loans and in particular, about my concerns that the loans aren’t getting to as many of the smaller businesses that need them. In this CNBC op-ed article, Elizabeth McBride and I pointed out how the face of entrepreneurship in the United States is changing. Specifically, the number of women-owned businesses has increased 31 times between 1972 and 2018 (in 1972, women-owned businesses accounted for just 4.6% of all firms; in 2018 that figure was 40%), according to the Kauffman Foundation. But the aid programs are largely failing to address the needs of these key entrepreneurial communities and the PPP loans are not getting broadly distributed across these demographics. The pressure on Main Street entrepreneurs is being compounded by the current economic crisis in ways that we haven’t even begun to wrap our heads around. Businesses started by women and minorities are more likely to have been impacted by the crisis and we fear will be the last to recover from it. According to the Center for Responsible Lending, a large majority of Black, Latino and other minority-owned businesses stand close to no chance of receiving a PPP loan through an SBA-approved bank or credit union. With loan sizes pegged to payroll, women and minority-owned businesses – which on average employ fewer people and as a result have smaller payrolls – are being de-prioritized by the banks that are the gatekeepers of the program. Compounding this problem, women and minority-owned businesses are also more likely to use contract or 1099 labor, which the PPP loan calculations exclude for purposes of calculating eligible loan size. And more fundamentally, these entrepreneurs are less likely to bank with an SBA approved lender. Even when they do bank with an SBA lender, there is evidence that these lenders are favoring their larger “small business” clients (for example, the average loan size in the initial PPP program was over $200k, representing businesses with payroll of around $1M / year).

I’ve published a number of posts over the past few weeks about some of the challenges of the existing PPP loans and in particular, about my concerns that the loans aren’t getting to as many of the smaller businesses that need them. In this CNBC op-ed article, Elizabeth McBride and I pointed out how the face of entrepreneurship in the United States is changing. Specifically, the number of women-owned businesses has increased 31 times between 1972 and 2018 (in 1972, women-owned businesses accounted for just 4.6% of all firms; in 2018 that figure was 40%), according to the Kauffman Foundation. But the aid programs are largely failing to address the needs of these key entrepreneurial communities and the PPP loans are not getting broadly distributed across these demographics. The pressure on Main Street entrepreneurs is being compounded by the current economic crisis in ways that we haven’t even begun to wrap our heads around. Businesses started by women and minorities are more likely to have been impacted by the crisis and we fear will be the last to recover from it. According to the Center for Responsible Lending, a large majority of Black, Latino and other minority-owned businesses stand close to no chance of receiving a PPP loan through an SBA-approved bank or credit union. With loan sizes pegged to payroll, women and minority-owned businesses – which on average employ fewer people and as a result have smaller payrolls – are being de-prioritized by the banks that are the gatekeepers of the program. Compounding this problem, women and minority-owned businesses are also more likely to use contract or 1099 labor, which the PPP loan calculations exclude for purposes of calculating eligible loan size. And more fundamentally, these entrepreneurs are less likely to bank with an SBA approved lender. Even when they do bank with an SBA lender, there is evidence that these lenders are favoring their larger “small business” clients (for example, the average loan size in the initial PPP program was over $200k, representing businesses with payroll of around $1M / year).

I recently published some recommendations that I sent to several members of congress to consider (some of these made it into the Federal Stimulus Package passed this last week). Included in it were some ideas that were specific to this point including the potential for a specific rural allocation of funds as well as including CDFIs in the program. I was happy to see that Congress specified $60 billion targeted at smaller banks (with the idea that these banks serve more small businesses). I was also happy to see CDFIs explicitly included in this 2nd traunch of the PPP program (these institutions are key avenues to funding these lesser served businesses). However, none of this is really enough, given the importance and relative size of women and minority-owned businesses in our entrepreneurial ecosystem. I plan to continue to work on this but I wanted to flag it to readers as an area of federal support that is significantly lagging. Unfortunately what hasn’t been addressed is the expansion of the program beyond “paycheck” and beyond the initial 8 week period of coverage that has initially been addressed. In the case of most main street and small businesses, calculations of payroll are far too small to provide the stabilization that these businesses need (many small businesses have expenses such as rent and utilities that are significant relative to their payroll costs). Further, by stipulating that funds need to be spend on payroll to qualify for forgiveness and by covering only an 8-week period, the current program effectively acts as a Federal unemployment insurance, rather than a business stabilization program. Companies need more flexibility in how they spend aid dollars to balance what’s in the best long term interest of their business (i.e., survival) and the best interests of their employees (many of whom will be out of work well past the 8 week period anticipated by Congress and some of whom are better off individually taking enhanced unemployment benefits).

Related to all of this, we’re putting on another webinar through the Financial Assistance Network (see the Network announcement here). We’re partnering with Good Business Colorado, The Bell Policy Center, Best for Colorado, as well as a number of other organizations and are especially targeting women and minority-owned businesses. You can register for the webinar here. I’d appreciate you sharing this with your networks to get the word out. The FAN network has already helped over 150 businesses but we have plenty more capacity and I’d like to see this number grow significantly, especially in light of the data that’s coming out showing just how many businesses haven’t been able to unlock federal aid and the number of companies struggling with key decisions that may literally effect their survival. Let’s give these businesses and the entrepreneurs behind them as much support as we can.

Why a 47-Year Republican is Crossing Party Lines and Lessons in Life and Business from Her Daughter’s Painful Journey

The post below was written by a friend who wanted to share it but asked to stay anonymous (so as not to call her mom out). I think it’s really powerful, I hope do you as well. The strain this political season is putting on families is real. November 3rd will be here soon, for better or worse…

Why a 47-Year Republican is Crossing Party Lines and Lessons in Life and Business from Her Daughter’s Painful Journey

I’m very close to my mother and I have deep respect for her. However, there’s been a nagging distance between us since Donald Trump ran for president four years ago.

My mother has been a loyal Republican for 47 years. I’m an Independent. We often voted differently, but we could almost always find common ground because we share many of the same values, most of which she instilled in me.

She raised me to be an independent woman and to believe that I could do everything that my brother could do. She taught me to be compassionate, to respect all races and religions, and to always take the high road. Whenever I faced conflict and wanted to lash out, she told me to “kill them with kindness.”

When Donald Trump ran for president in 2016, I was sure she would cross party lines to stand for the values that she taught me to believe in. To my surprise, she did not.

Then, the infamous “Grab her by the” Access Hollywood tape surfaced. I was certain that this would change my mother’s mind. How could my mother, a woman who raised me to be a strong, independent woman, support a man who so viciously objectified women? Yet, she stood by him. She admitted that his behavior was disheartening, but excused it because he was a “man of a different generation.”

I mustered the courage to tell her how disappointing that was for me to hear. I revealed that when I was 16, I overheard my bosses engaging in similar behavior as we saw from Trump in that video. As a result, it took me ten years to overcome my fear of being alone in a room with any of my male colleagues or superiors. It wasn’t until I heard that tape that I felt that same feeling of fear and sadness that had taken me ten years to overcome. To hear this from the man who may be the next president of the United States and to know that my own mother was supporting him was hard to swallow.

She cried and said that she was so sorry that I had that experience. She then shared a story about how her father’s friend brutally sexually harassed her in front of my grandfather and my father shortly after they were first married. Neither my father nor my grandfather stood up for her. That, as you might imagine, was deeply hurtful to her, but she said that she was able to forgive them because they, like Trump, were good men who simply came of age in a different era.

Shortly before the election, she called to let me know that she had made her final decision to vote for Trump and that, while she was ashamed to admit it, she realized that she “was not ready for a female president.” In that moment, I realized that the woman who had raised me to believe that I could do anything my brother could do did not actually believe that to be true. While my instinct was to lash out, I swallowed my tears and thanked her for the tremendous amount of courage it must have taken for her to make that call.

In the four years since then, I had many more urges to lash out. I always stopped myself because my relationship with my mother is more important to me than winning a political argument. I even started to appreciate the opportunity to be so close to someone with political views so different than my own, and to admire her ability to stand by her convictions. There was this one moment when we were sitting with eight other people who just assumed that she had voted for Hillary Clinton. This woman started going on and on about how she just couldn’t understand how people could be so ignorant and selfish to even consider casting a vote for Trump. I watched my mother squirm in her seat for a few minutes until, finally, she took a deep breath and said, “I just want you to know that I voted for Trump and I don’t believe I did so for ignorant or selfish reasons.” The woman apologized, and my mother proceeded to calmly and respectfully explain why she had voted for Trump. We all emerged from that conversation with greater compassion and understanding for both sides of the aisle, and I was deeply proud of my mother. I watched her interact with people with opposing political views on many occasions without ever muttering a hateful word. I’m proud to say that we never shared a hateful word about each other, until the first presidential debate of 2020.

As I watched the debate, I thought about how horrified my mother would be if her four-year-old grandson emulated the behavior of our president. I composed an angry email to ask her how she could possibly be so stubborn and stupid, and to tell her that I would never forgive her if she voted for him. Because I’ve learned to never send an email when I am below the line, I decided against sending it.

The next morning, she called me to ask for my advice. She had spent her morning working out with her 75-year-old trainer, who is recovering from cancer, at a gym where masks are required by state mandate. She asked a woman who was not wearing a mask if she would consider complying with the law, and the woman aggressively lashed out at my mother, stating that it was her gym, too, and that my mother had no right to police her. It spiraled into a dramatic 45-minute argument that involved the manager and several gym patrons. She called me to run through all of the facts and content of the argument, and I told her that none of that mattered because the woman was reacting emotionally rather than rationally. I gave her some tips on how to relate emotionally without evoking defensive behavior and then I said,

“Mom, I am afraid we will all continue to experience more incidents like this if we elect a president who promotes bullying and aggression.”

The next morning, I woke to a Facebook notification with this post from my mom:

“My daughter said something to me yesterday. A vote for Donald Trump is promoting the example that a person who behaves and conducts themselves as he does can rise to be the most powerful leader in the world. I have been a Republican for 47 years, but I will be casting my vote for a kinder, gentler candidate.”

As I reflect on this five-year journey, I am struck by how much I have learned and how applicable these lessons are to all aspects of my life. Because, as entrepreneurs and VCs, we are in the business of changing behavior and disrupting the status quo, I thought it might be helpful to share some of the tips I learned along the way.

People respond poorly to shame. The more self-righteous I became, the more she retreated.

Understand your own patterns and the patterns of those around you. I’ve been on a parallel path to become more self-aware to deepen my knowledge of Conscious Leadership. This paid dividends to my business and to my conversations with my mother. The Enneagram and the Four Tendencies have also been particularly helpful.

Build close relationships with people with opposing viewpoints. This journey with my mother has helped me approach all sorts of opposing viewpoints with more compassion and empathy, and it has led to much more productive conversations.

The reason people give is rarely the real reason for their decision. Over the past five years, it became increasingly obvious that my mother’s behavior was driven by conscious and unconscious gender bias, and 65 years of programming herself to believe that the path to a virtuous life was to be a good Republican.

Uncovering the most important behavior driver is the key to driving change. At the end of the day, I believe my mother made this decision for me. Above all else, she is a mother who would do anything for her children. I think our journey would have been much shorter if I would have recognized and tapped into that from the beginning.

Never send an email in a state of anger. I am not sure why the mask incident was the straw that broke the camel’s back, but I am certain that had I sent that below-the-line email to ask her how she could be so stupid and stubborn to support Donald Trump, she would have cast her vote for Donald Trump.

During COVID, I’ve been asking myself what I want to be able to say about how I spent my time during this pandemic. I think I finally have an answer. I want to learn how to better resolve conflicts and drive change without evoking hatred and defensive behavior from the other side. I learned a lot from this five-year journey. I want to take what I’ve learned to drive far more change in far less time. I hope this story will help you do the same.

Calling Financial Innovators

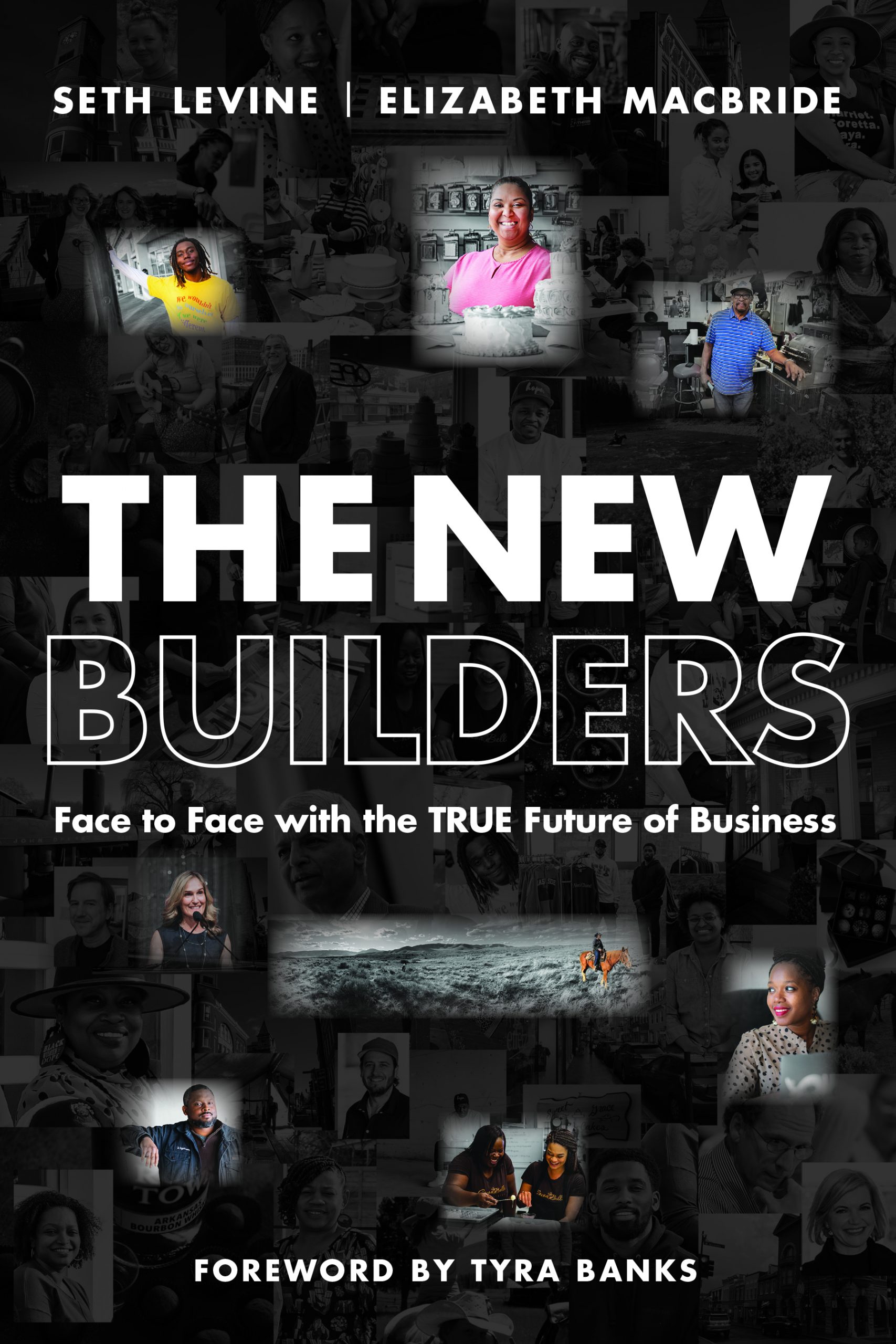

The Kauffman Foundation published an article last week that my New Builders co-author, Elizabeth MacBride, and I wrote about the inspiration for writing the book and – related – about how our systems of finance and support need to evolve to meet the needs of today’s entrepreneurs. One of our biggest inspirations and favorite New Builders is Danaris Mazara of Sweet Grace Heavenly Cakes. Sweet Grace was born in 2008, as the Great Recession ripped through the United States, particularly affecting working-class communities like Lawrence, Massachusetts where Danaris lives. She can identify the exact minute the bakery was born. She had $37 in food stamps to her name. “What are you going to do with $37 in food stamps?” Danaris asked herself. Danaris believes in God, and at that moment a divinely inspired thought came into her head: “Make flan.” From that beginning, her business was born.

Based on our research and the conversations we had in the course of writing our book, we believe there are countless potential Denarises out there. We need to find them and support them.

There’s a forgotten history of entrepreneurship in America, which includes many more women and people of color than is generally recognized. And the rates today at which women and people of color are starting businesses have accelerated to the point that, today in America, white men are now the minority of business owners.

The demographic shift is due to the growing diversity of our country, but also reflects some special conditions that make startup life and small business ownership especially appealing to women and people of color. Given the economic needs driving them, we’re seeing a surge in business starts post-pandemic.

Lacking the entwined systems of finance and mentorship that supported past generations of (white, male) entrepreneurs and that still over-index in support of a tiny subset of businesses in the tech world, today’s entrepreneurs face almost insurmountable obstacles. Entrepreneurship in America has been on a slow decline for the past 40 years but very few people in the mainstream notice this trend.

But it is the decline in the broader world of entrepreneurship that is a crack in America’s identity as a land of opportunity and innovation. Innovation doesn’t come soley from white men educated at Ivy League schools. Innovation comes from giving a broad swathe of people the opportunity to create businesses that drive economic growth.

We believe the fastest lever to give people like Danaris the wherewithal to start companies is a well-designed system of finance that provides capital, as well as the emotional and social support entrepreneurs need. According to Kauffman Foundation research, beyond the 1% of startups receiving venture capital financing, only about 17% take any outside financing at all. The key is getting the same level of robust financing to the remaining 83%.

There are four promising directions in finance innovation that would help the vast majority of entrepreneurs who aren’t getting funding. There are many more to consider, but these would be a good starting point.

- Financing at scale. Large technology platforms, like PayPal and Stripe, have the potential to touch many businesses but the rates charged are higher than those found at banks, and they fail to offer the kinds of other support that are arguably even more important to success. If they were to become leaders in the movement to help New Builders, it would have to come about because of a mindset shift among their executives and the largely white men in their networks: that businesses started by women and people of color are not inherently riskier than the companies created by men, and that New Builders are not environmental, social and governance (ESG) investments. And these executives would need to accept their responsibility for creating a more inclusive and equal society.

- Create a new capital class. Empowering more people to see themselves as investors and lenders would unlock more capital at the grassroots level. How could this function in communities and Main Streets in America? It’s not clear yet but we believe there are innovations to be had in enabling more people to invest in startups. If more people think of themselves as investors, they will create demand for new financial products.

- Connecting investors with Main Street. Community loan funds have existed for decades, enabling community-minded institutions and wealthy individuals to put money into funds that in turn provide capital and support for businesses. Are there ways to scale these funds or turn them into an asset class? There are already signs that technology is at work in this space, as a handful of new companies, like Mainvest outside Boston, build platforms that help people who aren’t necessarily wealthy, invest in companies in their communities. The regulations in this space are still onerous, however.

- New Builders helping New Builders. One of the most promising developments coming out of the increased social justice awareness in 2020 has been a focus on getting more capital into the hands of Black and brown innovators in finance. The $100M fund-of-funds partnership between the Kauffman Foundation and Living Cities is one example of this.

The New Builders is in many ways a call for people who now control capital in our country to do what they do best: innovate new financial products to create and serve a new market. We should be asking ourselves how we can adapt to the new generation of people who are starting businesses today.

There are hopeful signs. While the most powerful members of the capital class can seem short-term and indeed are often deeply motivated by profit, they want to be ahead of the game. The future of the economy clearly lies with New Builders, who are more diverse in terms of their background, but just as capable and lofty in their dreams as any generation of entrepreneurs before them. I have faith that we’ll find new and creative ways to help them succeed.

Startup Communities | Rural Entrepreneurship

I’ve always loved Brad’s Startup Communities – it’s long been my favorite of his books, built upon ideas that are clearly stating the test of time. In it, he talks about the key ingredients to building a startup community and talks about our experience in Boulder – one of the first startup communities to really thrive outside of the traditional tech hotbeds of the coast (but certainly not the last). He’s recently come out with a new version of the book, as well as a companion book called The Startup Community Way. They are outstanding.

I’ve always loved Brad’s Startup Communities – it’s long been my favorite of his books, built upon ideas that are clearly stating the test of time. In it, he talks about the key ingredients to building a startup community and talks about our experience in Boulder – one of the first startup communities to really thrive outside of the traditional tech hotbeds of the coast (but certainly not the last). He’s recently come out with a new version of the book, as well as a companion book called The Startup Community Way. They are outstanding.The Importance of the Democratization of Capital

The democratization of capital may be messy at times, but it’s much better than the alternative. And it’s long over-due.

The democratization of capital may be messy at times, but it’s much better than the alternative. And it’s long over-due.

Robinhood’s actions to restrict trading in GameStop stock, as well as several other issuers, was completely the wrong response to an increasingly active capital class. It’s time to give up this old notion that small investors somehow need to be saved from themselves (as they claimed was the reason they halted trading in GME and other issues *). For years, capital investment has been the sole purview of the wealthy in the United States and elsewhere. We’ve long had a series of laws that restricted people’s abilities to invest in private stocks and at that same time, given fee structures and the general opaqueness of the public markets, it’s generally been the purview of only wealthy Americans. Both of those trends have started to change over the last handful of years – trends we should be encouraging not limiting.

The Jobs Act, passed in 2012, was a positive step in opening up private investment to more Americans. Title III of the JOBS Act (which was adopted in 2016) lets startups raise money from non-accredited investors. Previously, investors had to income (at least $200,000 a year over) and/or net worth (at least $1 million excluding your home) to be considered “accredited” and allowed to invest in any number of private assets. Title III allowed anyone to invest via equity crowdfunding. There are some challenges to Title III that still need to be addressed. For example, companies are limited to raising just over $1M million through this method, which limits the scope of businesses that can take advantage of capital formation in this manner. Additionally, there isn’t a mechanism for individuals to create “funds” under Title III to spread out their investment risk (they can only do so by investing project by project). Perhaps most importantly, there are significant per investor limits on their ability to participate in Title III Crowdfunding offerings that limit individual investor participation in crowdfunding marketplaces. But, opening up the ability to invest to a broader swath of Americans – democratizing capital – was a positive and long overdue step. At the same time on the retail side, platforms such as Robinhood have opened up public markets trading to more and more people eager to gain a foothold in the markets. To me, these trends are incredibly positive.

Capital ownership should be more broadly distributed. And while there need to be sensible regulations in place to prevent fraud, the notion that somehow people with less than a certain threshold of net worth can’t make intelligent investment decisions in the private markets is absurd. Robinhood restricting the trading of these stocks is just a continuation of old thinking. They’re a capitalist platform. They should believe in the capital markets and that, even if there are short term aberrations, ultimately the markets will figure it out. The fact that their actions helped stem a short squeeze that was hurting larger Wall Street traders and hedge funds exacerbates the perceptions that they’re not truly democratizing capital in the way that they have suggested that they are. Fred Wilson wrote a similar post earlier this week that I strongly agree with and would highly recommend reading as well. The solution to these sorts of aberrations in the market is to let the market play them out. In the long run, efficient markets will do exactly that (find the efficient price) and the long-term value of the stock will eventually trend back to its underlying and intrinsic value.

* It’s worth noting that while Robinhood claimed they stopped trading to “protect customers” the true reason was perhaps a bit more complicated. After admitting that there were some “regulatory issues” that prompted the trading halt, the company eventually revealed that the company itself lacked the liquidity (capital) required to allow trading to continue at the levels it was seeing. It subsequently put together a hasty $1bn financing.

Fight for your rights! American Censorship Day (that’s today!)

Today Congress is holding hearings on what, if passed, would effectively become a censorship system for the internet. The threat comes in the form of two bills, currently making their way through the legislative process – Protect IP Act (PIPA – S.968) and Stop Online Piracy Act (SOPA – H.R.3261). Below is a video that describes the bills and their potential impact (and you can read more at http://americancensorship.org/):

PROTECT IP Act Breaks The Internet from Fight for the Future on Vimeo.

The effective censorship of websites (by blocking or slowing access to them) is what I find particularly disturbing. We already have a fundamental access problem on the internet. As internet access becomes increasingly important to society – truly part of the fabric of our democratic society – lack of access to the internet (and lack of high speed access) is becoming an increasing social and economic issue. Lack of internet access contributes to an increasing gulf in our society. And it’s a problem that government has recognized – for example when it required Comcast to offer low income households favorable rates on internet access in exchange for granting approval to the Comcast/NBC merger. I’m not arguing (at least in this post) for some kind of universal service fund for broadband access (and as a “capitalist” by title, I hope that the primary solution to this can be a market driven one). I’m pointing out that we already have some challenges around access to the internet that we haven’t even addressed. And now we’re talking about layering on an access hierarchy on the other side of the equation. The vast majority of the increase in the productivity of the american worker that we’ve seen over the past few decades has been driven by technological innovation (we’re working smarter, more than we’re working harder). Do we really want to take a primary driver of that technology innovation – the internet – and set up a system that effectively stifles the ability of new companies and new technologies to reach users? A system that rewards the embedded power structure of big business in the United States? I’m not arguing in favor of web piracy. I’m arguing for common sense. And against trusting the people who sued to block the VCR and MP3 players from coming into existence (two technologies, which they later ended up significantly benefitting from) by giving them the power to effectively shut down new businesses and censor our access to new technologies.

There’s a reason that the backbone of the internet is governed by “peering” relationships. We’re all peers on the internet. Let’s not forget that.

Accidents in North American Venture Capital

As a member of the American Alpine Club I look forward each year to the arrival of my copy of Accidents in North American Mountaineering. This is a book that the club publishes annually that documents climbing and mountaineering accidents that are reported each year in the United States and Canada. The idea, of course, is to educate the climbing community on things that can go wrong in the backcountry in an attempt to make everyone safer (as if the threat of dying were not enough, we also have to worry about being written up in Accidents. . . ). A typical entry might be titled: Fall on Snow – Unable to Self-Arrest, Faulty Use of Crampons and would then go on to describe how someone fell on a snowfield (in this case not far from Boulder, CO), dropped his ice-axe and wound up breaking his legs when he inappropriately tried to stop himself with his crampons (ouch!). Other titles this year were: Stranded, Exposure-Hypothermia, Inadequate Clothing/Equipment, Climbing Alone, Weather, Exceeding Abilities (apparently this guy got it all wrong); or my personal favorite: Stranded, Exceeding Abilities, Incompatible Partners – Poor Communication (I like that having crappy partners is an official designation of the AAC).

As I thumbed through Accidents this year it occurred to me that it would be great to have a venture capital version of this book. Entries could be titled things like: Poor Sales Execution, Faulty Use of Partners, Inability to Raise Additional Financing. Or for a company from 1999: Inexperienced Management Team, Poor Market Timing, Superbowl Ad. Or perhaps: Product Shortfalls, Slow Customer Traction – Inability to Cut Costs Quickly, Inattentive Investors. I assume that most VCs think a lot about companies that didn’t work out and why – this would be a way to memorialize that effort and to share it across the community. I’m actually ½ serious here – let me know what you think.

Immigration policy for recent grad school grads

I made reference to the issue of immigration policy in a post last week (see “Want more jobs? Support Entrepreneurship”). In that post I referenced a WSJ OpEd piece that my partner Brad Feld wrote last week with Paul Kedrosky about the Start-up Visa Movement (the idea that we should make it easier for foreign born entrepreneurs who are starting their companies and who have obtained financing to stay in the United States to build their businesses). In my post I went on to say:

But let’s take this idea further. For example, how could it possibly make sense to deport a recent graduate school graduate (someone with the kind of technical degree that we so badly need here in the US and who received significant federal and state subsidies to study here)? We should be doing everything we can to keep smart, educated, motivated immigrants here – we want them contributing to our society and to our economy.

Susan Hockfield has a great OpEd piece in this morning’s Journal on this exact topic that is well wroth reading. Here’s my favorite quote from the article to give you the flavor but please click through and read the whole thing.

Our immigration laws specifically require that students return to their home countries after earning their degrees and then apply for a visa if they want to return and work in the U.S. It would be hard to invent a policy more counterproductive to our national interest.