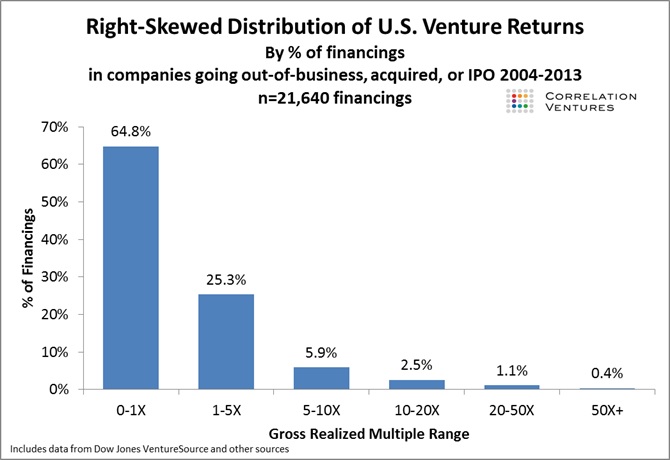

A few years ago I wrote two posts – Venture Outcomes are Even More Skewed Than You Think, and Some More Data On Venture Outcomes – that challenged the mythology that only 1/3 of venture-backed deals failed and showed just how rare large (10x and greater) venture returns really are. I think the sharpness of the curve surprised a lot of people and contributed to a bunch of discussion at the time around just how rare “venture outcomes” really were. Not surprisingly, I was looking at the data through the lens of an investor and in so doing was only focused on how well investors fared in company exits (as a side note, I’m hoping to update these data now that a few more years of a bull market are behind us).

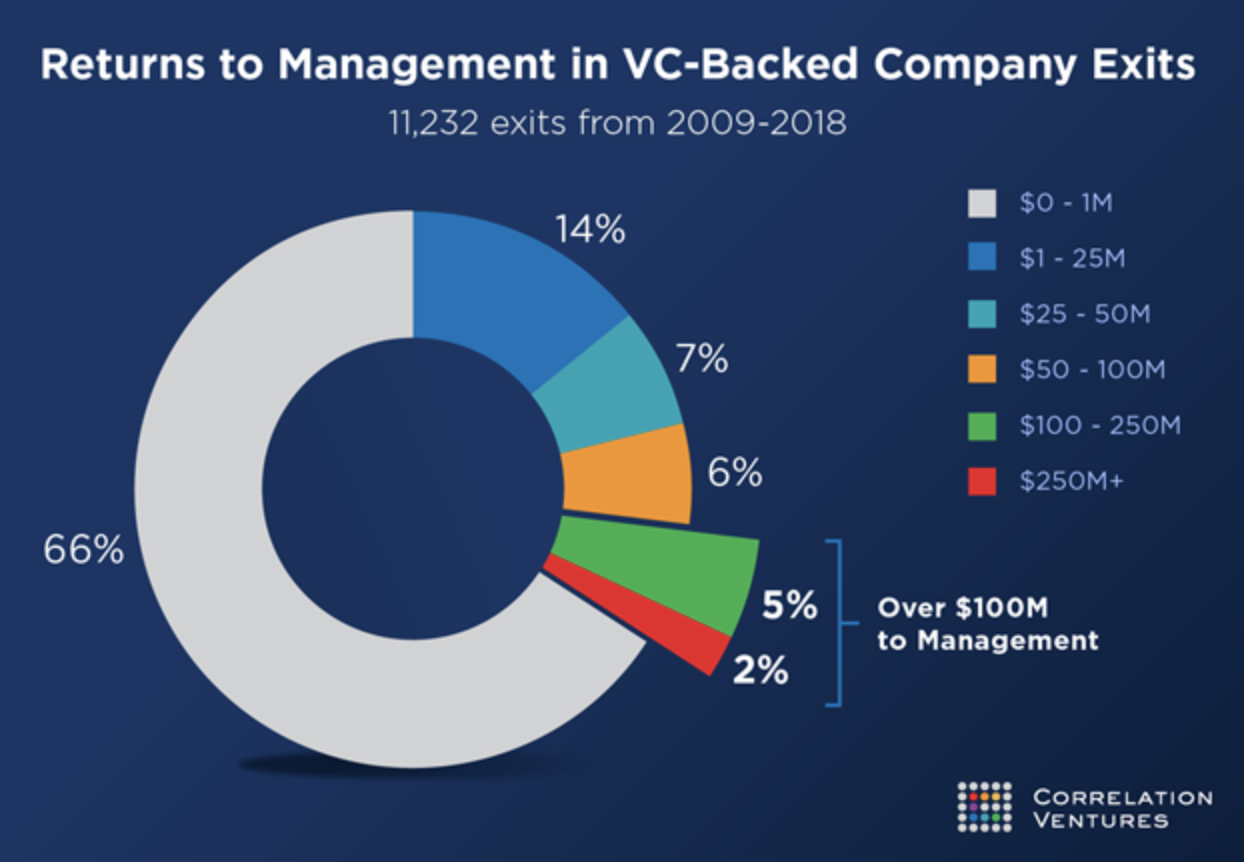

The data that underpinned the analysis was from Correlation Ventures, which is a fund that invests programmatically behind certain investment signals – thus the large database of transactions. A few months ago they put out another interesting piece of analysis that I thought was worth highlighting here (Trevor’s original post can be found here). In this latest post, they’re taking a look from the perspective of management teams – how much do they make when a company exits. In this case they defined “management team” as founders and C-level executives. And exit was a sale of the business, IPO or wind-down. The data set included over 11,000 events from the 10 year period between 2008 and 2018.

I thought the data were encouraging.

Not surprisingly, 66% of the time, management made very little (less than $1M) – I say not surprisingly because this generally maps to the venture side of the analysis, where roughly the same % of investments failed to return capital. In 20% of the outcomes, management teams made more than $25M. 7% of the time they made greater than $100M. The full details are below. I’ve also copied the graph from my original Venture Outcomes post so you don’t have to click through to see the equivalent data from the venture perspective.

Clearly, the risk of starting a business is high, but management success is generally aligned with investor success (although remember, taking venture isn’t for everyone). There are plenty of ways that management incentives are not aligned with investor incentive (the most often talked about and obvious one being that investors place many bets while management teams place a single bet in the company they’re working for; this has been somewhat mitigated by the shared equity pools and, more so, by the advent of funds that help employees exercise their options when they leave a business so they can keep much of their upside as they move from job to job).

But at a high level, when companies do well, management teams do well. Which is good to see some data on.