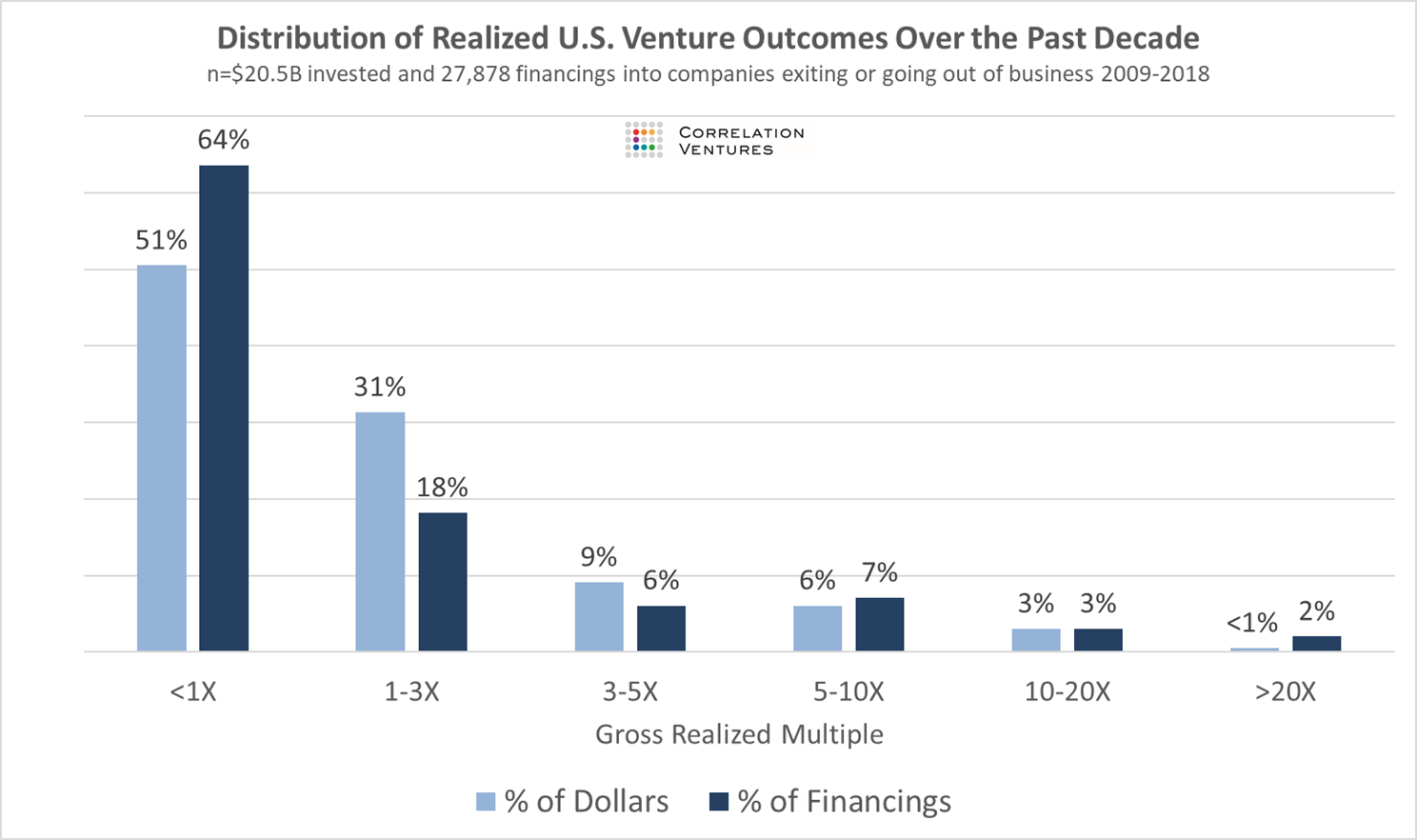

Some of the most popular posts I’ve written over the past couple of years were the two that focused on just how rare outsized returns for an individual deal are in venture capital. You can see the original posts here and here. In those posts I was analyzing data from Correlation Ventures that showed just how skewed venture returns are, specifically that 65% of investment rounds fail to return 1x capital and only 4% return greater than 10x capital.

Ian Hathaway, who recently co-authored the second edition of Startup Communities with my partner, Brad, sent me the chart below which highlights how that translates to returns in venture capital as an asset class. I’ve seen versions of this chart before and while it’s not surprising it is always jarring to see it laid out like this. Specifically, the difference between the best performing and average performing firms are incredibly wide. Venture is a hits business and if you think about a typical venture fund of almost any size having somewhere between 25 – 40 investments, the chances of any one of those investments being a true outlier and returning a multiple of the fund are quite small. In order to have a successful fund, it’s almost a requirement that you have an outlier return for at least one of your investments (see below the chart for the math).

Some quick math highlights why this is the case. For example, assume a $100M fund with 30 investments. That’s a little over $3M per investment, and while there is some dispersion from the average across companies in a fund, it’s not a bad way to model it. But from the outcomes chart above (the first one) we know that on average only 1 (actually just fewer than 1) company in that group of 30 will return between 10x and 20x. And less than 1 will return 20x or greater (I’m using the company averages, the dollar averages are on a per round basis, which would make these numbers even worse). A 20x returner for a fund that on average invests $3-$3.5M in a company doesn’t return that fund. Taking the most aggressive end of these numbers would still only have this one company returning 70% of the fund’s capital. If you were going to have several of these, of course, that would work out for your fund. IRR will depend on the timing of cash flows but as a quick rule of thumb, venture funds look to return at least 3 times the invested capital – after fees, so more like 3.5x on a gross basis. That’s pretty hard to do without a true outlier return (50x+) and/or consistency of 10x+ returns that is simply hard to generate. And here’s where the dispersion comes in. The best funds do have multiple companies that return in that range. Or higher. But that means the median fund doesn’t have any. And that is why the average venture fund isn’t actually a particularly good investment and also why so many venture funds fail to return capital.

I thought about this a couple of years ago when I wrote about the optimal venture fund strategy and my conclusion was that venture firms should place more bets and have more exposure across a larger set of businesses. Obviously, those inside the industry argue that managers who are good at picking businesses would do better to own more of fewer businesses if they can show that they have the aptitude to invest in those that become true outliers. But given how rare they are, I wonder if that is arguably the optimal strategy. As David Cohen replied once years ago when I asked him what the key to being a successful venture capitalist was: “Luck”.